Building a Payday Loan App That Cuts Approvals From 48 Hours to Minutes

A registered South African lender came to us with a regulated product and a tight deadline. They needed an instant payday loan app where every loan decision is traceable, every role has boundaries, and every borrower sees their credit score trend. Here's how LITSLINK built it.

- → Increased agent throughput 3x (from 25 to 75 apps/day)

- → Cut approval cycle from 24-48 hours to minutes

- → 5 PM daily cut-off for same-day funding to the in-app virtual card

Project Details

Our client is an independent short-term lending operator working under the National Credit Regulator licensing in South Africa. They came to LITSLINK with a fully manual lending pipeline, a Rand-denominated borrower base, and a deadline tied to the next quarter. The brief was specific: ship a mobile-first product with a four-role back office, and do it before competitors closed the gap.

Business Challenge – A South African Lender Ready to Scale

The lender ran a manual operation. Bank statements came in as email attachments.

An agent picked them up, copied numbers into a spreadsheet, ran the affordability check by hand against National Credit Act thresholds, and then phoned the borrower back.

Average turnaround sat between one and two days. In a market where same-day cash is the entire value proposition, that gap was a structural problem.

Paper-shaped digital

Documents were digital only in the sense that they traveled by email. Verification still happened by eye, on a screen, line by line. Roughly thirty per cent of agent time went into matching attachments to applicant names.

No single view of the customer

Loan history, credit score movement, and disposable income lived in three different places: a CRM, a credit bureau export, and a payroll spreadsheet. Decisions were being made on partial information every day.

Role confusion across the funnel

Agents, managers, and administrators asked questions that the existing system couldn't answer for itself. Every escalation became a phone call, and every phone call cost an application that walked over to a competitor.

Technologies Behind the Payday Loan Software

Our Payday Loan Software Solution

The brief was specific. Build an instant short-term lending tool – closer in feel to a personal loans flow than to a traditional bank facility – that takes a borrower from sign-up to approved cash inside a single session, before the 5 PM daily cut-off. Surface the same dataset to staff with the right permissions, and only the right permissions.

We started with the document moment. That’s where the old process died. Borrowers had to upload three months of bank statements and a recent payslip, sign the credit agreement, and tag their employment. The onboarding screen titled “Make it online” was the first thing we prototyped. It had to feel light. Three taps to upload, one to sign, no jargon – that was the rule.

The architecture followed the four roles. A borrower app on iOS and Android shared a Node.js back end with a web dashboard for agents, administrators, and managers. Each role saw a different slice. An agent could approve a loan up to a defined ceiling. An administrator could change that ceiling. A manager could pull reports on the whole portfolio without touching live records.

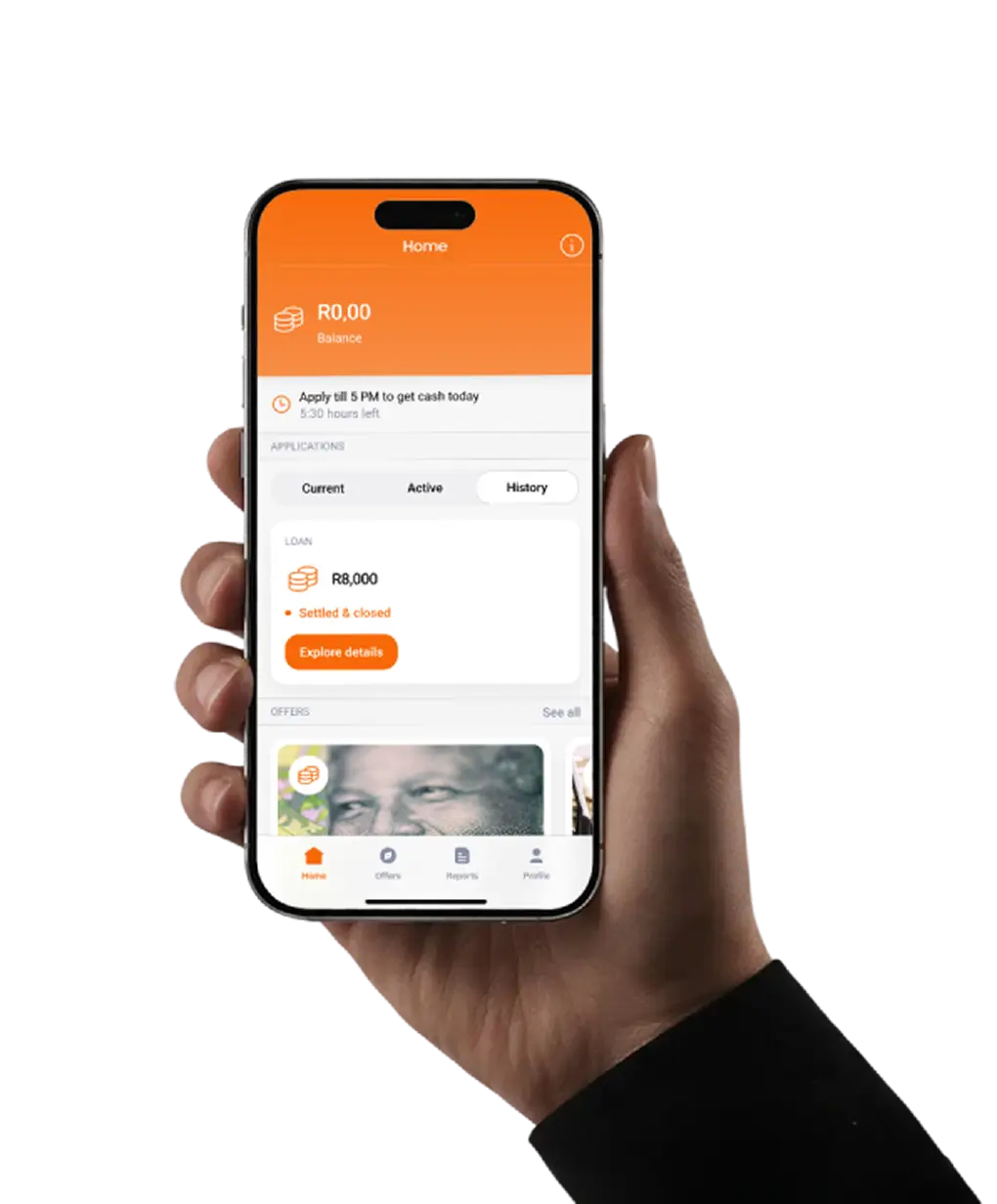

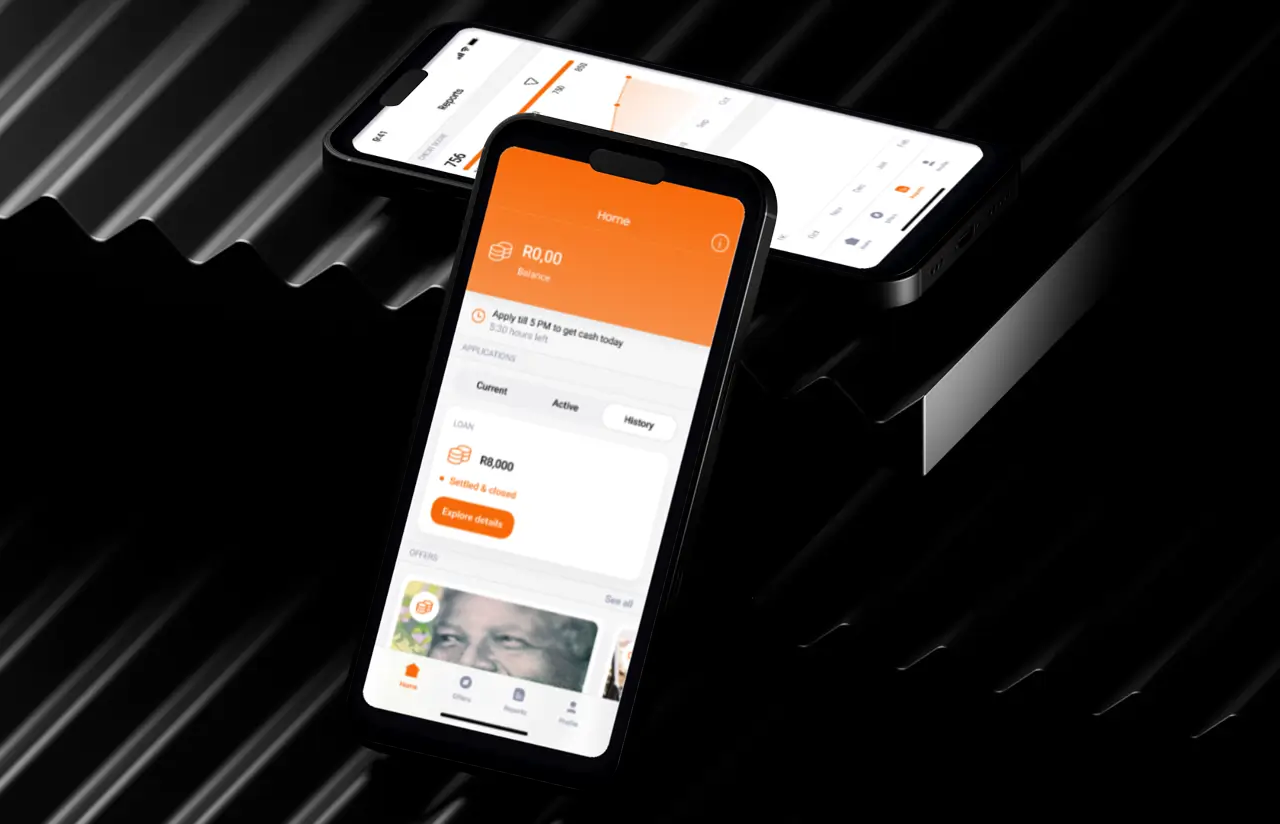

Push notifications carry the urgency. “Apply till 5 PM to get cash today” sits at the top of the home screen with a live countdown – five hours thirty left, three hours left, until the badge flips to “tomorrow.” Borrowers don’t have to know the rule. The rule knows them.

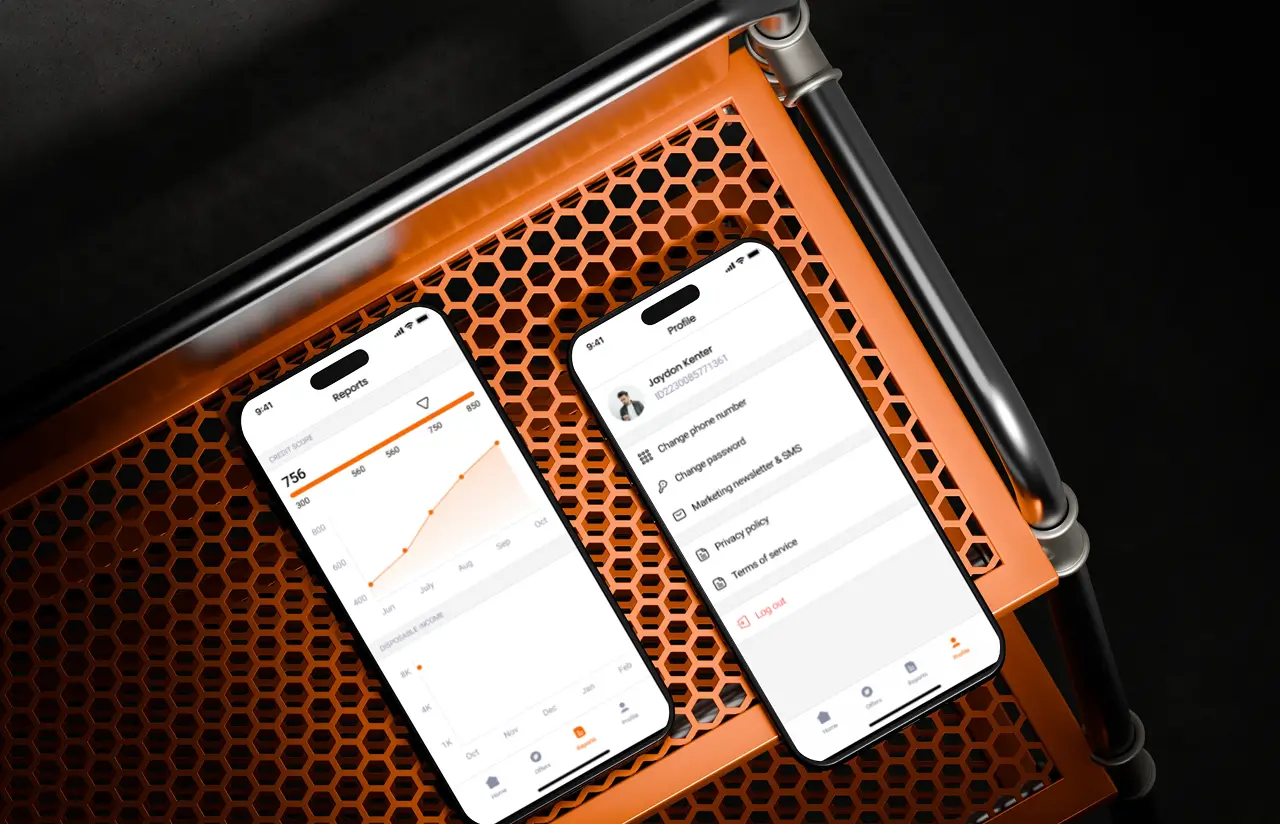

Credit scores got their own screen. The report’s view shows the score (between 300 and 850, matching the local bureau range) on top of a six-month trend line, with disposable income plotted underneath so the borrower can see the relationship between the two. The aim was simple: stop the guesswork.

None of this is an off-the-shelf wrapper around a generic lending API. South African regulation – affordability assessments, DebiCheck mandate rules, NCR disclosures – is wired into the loan calculator itself, not bolted on at the end. An app that makes loaning safer for both sides works only when those rules are baked in by design.

Document onboarding before lunch

Borrowers upload three months of bank statements and the latest payslip from the phone camera, sign in-app, and see a verification status within ten minutes. No paper trail. No email back-and-forth.

Five-PM cut-off countdown

A live hours-left indicator sits on the home screen until the daily window closes. Submit before five, and the funds land the same day. After five, the messaging shifts to tomorrow on its own – borrowers come back the next morning.

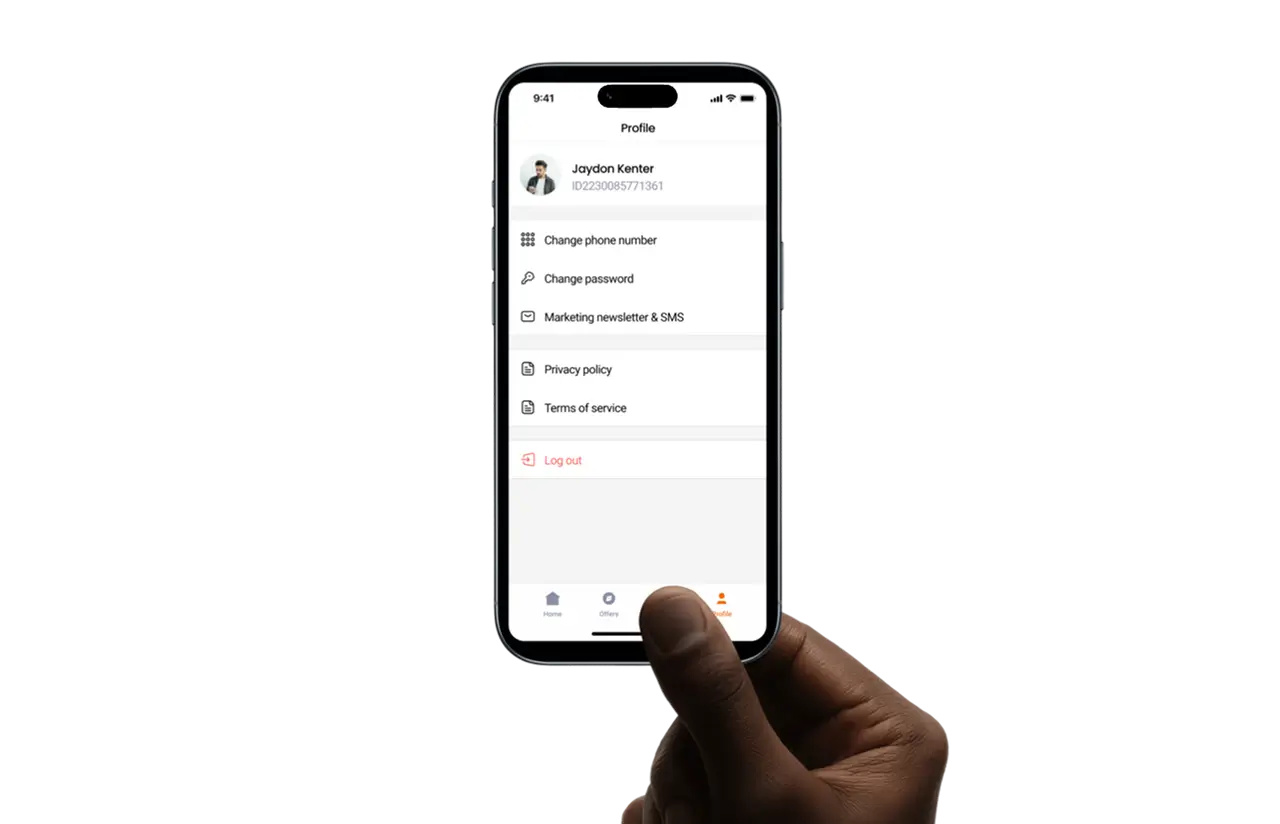

Four-role permissions out of the box

Borrowers, agents, administrators, and managers each see a tailored view. An agent approves. An admin re-tiers. A manager pulls a report. No one touches what they shouldn't, and audit logs catch what they did.

Virtual card on issuance

Approved funds load to a virtual debit card inside the wallet – number, expiry, CVV – usable wherever a debit card works. No trip to a branch, no plastic in the post, no waiting for a courier.

Credit score view that explains itself

A 300–850 dial, a six-month trend line, and disposable income plotted alongside. Borrowers stop guessing why the number moved. They start seeing the cause.

DebiCheck-compliant repayment schedule

Repayment dates align with the borrower's confirmed payday under South African DebiCheck rules. The schedule renders inside the app the moment the loan is signed, not three days later.

Scrum Methodology

Project Journey – How We Built the Payday Loan Platform

The plan was short on paper and tight on time. Five sprints, two weeks each, four user roles to ship, two app stores to clear. We kept the cadence steady and pushed the riskiest piece – the role-aware approval workflow – into the middle of the schedule, not the end. That way, if it broke, we had two sprints left to fix it.

How the payday loan app works

- A borrower opens the app, uploads three months of bank statements and the most recent payslip, then signs the credit agreement in-app – all in one session.

- The back end parses the statements, runs the disposable-income calculation against National Credit Act thresholds, and surfaces a verdict on the same screen the borrower is sitting on.

- First-time borrowers can access up to R8,000; returning clients with a clean history, up to R12,000. Limits subject to NCA thresholds at time of launch.

- An agent sees the application in the web dashboard, checks the flagged fields, and either approves or sends back for clarification – with a status update fired in-app within seconds.

- Approval triggers funding to the in-app virtual card. Number, expiry, CVV usable the same minute, wherever a debit card works.

- A DebiCheck mandate pulls the agreed amount on the borrower's confirmed payday. The schedule lives inside the app – one less screen for the borrower to chase.

Scrum Process Flow

Mobile application development of the sort short-term lenders need does not reward big-bang launches. Scrum’s two-week cadence meant the credit risk lead had working software to argue with every fortnight. Three of the five sprints shipped with revisions that came directly from those Friday reviews – and one rounding bug got caught before it left the building.

-Timeline

Five Phases of Delivering the Payday Loan Solutions Platform

Auth & Onboarding

- Role-based access for borrower, agent, administrator, and manager, built on Auth0

- Account creation with phone OTP plus email verification

- Borrower onboarding: documents, signature, ID verification in one flow

Loan Flow

- Loan calculator with NCA-compliant affordability check baked in

- Repayment schedule rendered the moment the agreement is signed

- Bank statement parser for the last three months – local format quirks included

Approvals

- Agent dashboard with an approval queue sorted by cut-off proximity

- Administrator panel for ceiling adjustments and role re-tiering

- Status notifications by SMS and in-app push, identical content on both channels

Reporting

- Manager reporting view with portfolio-level metrics (volume, default rate, score trend)

- Loan history view with the 300–850 credit-score chart anchored on the home tab

- Push notifications for repayment dates and personalized offers

QA & Launch

- End-to-end tests written for each of the four user roles, run before every release branch

- App Store submission, one privacy disclosure fix, resubmission within 48 hours

- Google Play submission with a phased rollout starting at 10% of users

UI/UX Design

Borrowers see a clean mobile screen: large type showing the loan amount, a countdown timer to the 5 PM cut-off right below the balance, and one primary action per screen. This layout increased application completion rates – users stopped dropping off mid-flow.

The admin side flips the priority. Agents get a dense tabular layout with contact cards on the left and finance-offer cards on the right. The added information density let agents process up to 75 applications per day – three times the previous rate of 25 – without screen fatigue or burnout.

Both sides share the same typeface, color tokens, and brand gradient, keeping the product visually consistent across borrower and back-office experiences.

Results

Before

- ✕24–48 hour approval cycle, with most decisions held up by document hunts

- ✕ Affordability checks done in a spreadsheet, then re-checked by phone

- ✕One agent handled ~25 applications a day before the queue overflowed

- ✕ No view across loan history, credit score, and disposable income in one place

- ✕Borrowers heard back by phone – sometimes after the daily cut-off had passed

After

- ✔Same-day funding for applications submitted before the 5 PM cut-off

- ✔In-app affordability verdict rendered within minutes of upload

- ✔~3× agent throughput, with the queue holding around 75 applications per day per agent, stabilized within the first month post-launch

- ✔One report view that puts loan history, credit score, and disposable income on a single screen

- ✔One push notification replaces the "did I get approved?" phone call – and the call after that

The Impact

-Verified Reviews

Our Reputation on Top Platforms

LITSLINK sits consistently among the top fintech and mobile software development teams on Clutch, GoodFirms, and DesignRush. Reviews call out the same three things – technical depth in financial software development, communication during a sprint, and the willingness to push back when a feature isn’t going to ship clean. We treat that pushback as part of the deliverable.

Have the FinTech App in Mind?

Need a payday loan app, a credit scoring tool, or something else in the lending space? Describe your project, and we’ll deliver an execution plan within 48 hours.